The Ultimate Guide to Buy and Build Strategy in Private Equity

Buy and build works when the platform protects the customer relationships it just paid for. Most buy and build strategies are run as an arithmetic exercise: buy a platform, staple on smaller companies, sell the combined business for more than the pieces cost apart. The deals that actually hold up are the ones where someone owns keeping every acquired company’s customers loyal through the integration, with that ownership tracked as closely as the revenue on the closing paperwork.

TL;DR

- Buy and build creates real value when relationships survive the deal. A bigger org chart is just a byproduct of that.

- Most platforms underperform because integration plans focus on systems and reporting lines and leave out the specific people who kept each acquired company’s customers loyal.

- Rank every add-on company by how sturdy its relationships are before you rank it by revenue. A small book of business tied to one salesperson is worth less than it looks.

- A value creation plan needs a named owner for every key account inside every company you buy, set before the deal closes.

- Operating partners should own the regular check-in that catches relationship trouble early. The acquired company’s own CEO owns the relationship itself.

- The first 100 days determine whether a newly acquired company’s customers stay or start taking calls from a competitor.

- Growing the business’s value and keeping customers loyal should be tracked on the same scorecard. One without the other is half a picture.

What is a buy and build strategy in private equity?

A buy and build strategy means buying one company big enough to serve as a home base in a scattered industry, then adding smaller companies to it over time to grow revenue, market share, and what the combined business sells for down the road, faster than either company could grow alone. The first company is the platform. The smaller companies bought afterward, usually called add-ons, get folded into shared systems, leadership, and back-office work.

Defined Term: Platform company.

The first company bought in a buy and build strategy, big enough to serve as the operating and management home base for the smaller companies bought later.

Defined Term: Add-on acquisition.

A smaller company bought after the platform and folded into it, typically to add customers, geography, or capability to the combined business.

The strategy has been popular in private equity for a straightforward reason. A scattered industry with no dominant player usually has dozens of small companies selling for a low price relative to their earnings, because they lack scale. A combined platform with more revenue and better management typically sells for a higher price relative to earnings. Buy three or four companies at 5 times earnings each, combine them into a platform worth 8 times earnings, and that math alone creates value before a single customer relationship changes hands.

That math is real. It is also the entire reason so many buy and build platforms disappoint.

Understand where buy and build sits among PE growth strategies

Buy and build is one of three common paths to growing a company you’ve bought, alongside organic growth (building demand and sales capacity inside the existing business) and market expansion (entering new geographies or customer segments with the existing product). Buy and build is the fastest of the three on paper, because it adds revenue through acquisition instead of waiting for it to build up on its own. It is also the riskiest, because every add-on brings its own customer relationships, and those relationships were built around a company that no longer exists in the same form.

Why do buy and build platforms underperform after the deal closes?

Buy and build platforms underperform when the integration plan consolidates each add-on’s revenue line without a parallel plan to protect the customer relationships behind it. The math behind most buy and build deals accounts for savings in procurement, back-office headcount, and shared systems. It rarely accounts for what happens to a customer relationship when the person who owned it for fifteen years now reports to a new CEO they have never met, using a system they have never seen, selling under a brand they do not recognize.

We call this the arithmetic-only platform: a buy and build strategy run purely as number crunching, where the deal math assumes revenue transfers automatically as long as the paperwork closes.

Defined Term: The arithmetic-only platform.

A buy and build strategy where the whole bet rests on combining companies and selling the package for more than the pieces cost, with no explicit plan for keeping each acquired company’s customer relationships intact through the integration.

Spot the assumptions buried in the deal math before they compound

Every buy and build deal has assumptions buried in its investment thesis about whether customers stick around. Pull them out and question them directly before signing. Ask: does this deal assume the acquired company’s top ten accounts stay at their current spend level three years out? Does it assume the founder or key salesperson stays engaged past the earnout (the period where part of the sale price is still tied to the business hitting its numbers)? Does it assume the acquired company’s brand can be folded into the platform’s brand without customers noticing? Write the answer to each question down. If the answer to any of them is “we’re just assuming it,” that assumption belongs in front of whoever signs off on the deal as the actual risk it is.

Track the specific ways integration breaks trust

Integration breaks customer trust in a small number of repeatable ways: the point of contact changes without a proper handoff, invoicing or service terms change without warning, the acquired company’s name disappears from correspondence before customers have been told why, or the founder who used to take every call goes quiet during the earnout. None of these show up on a cost-savings tracker. All of them show up eighteen months later as a lost account with a note that says “moved to a competitor” and no clear reason why.

What actually creates value in a buy and build platform?

Value comes from keeping every acquired company’s customer relationships intact while the platform combines their systems, reporting, and management underneath. Revenue is the byproduct of doing that well. Skip the relationship work and the revenue is what leaves first, usually quietly, one renewal at a time, long before it shows up as a miss in the quarterly numbers.

This is the piece most buy and build deals get backward. Companies get ranked by revenue size and growth rate, and the pre-deal check treats relationship risk as a box to tick before signing, when it needs ownership that continues well past close. A small book of business concentrated in two accounts, both of which trust one salesperson who has one foot out the door, is a worse asset than a larger book spread across fifteen accounts with documented relationships at multiple levels. The revenue numbers on the deal paperwork do not show that difference. A map of who actually owns each relationship does.

Rank each add-on by how sturdy its relationships are before you rank it by revenue

Build a simple scoring table for every company under consideration or already inside the platform. Score each on three things: how much of the revenue sits with the top three accounts, how many people at the company have a real relationship with those accounts versus how much rides on one person, and how much of the account history is written down versus how much only lives in someone’s head. A company that scores well on revenue and poorly on all three of those factors needs a plan to steady its relationships before it needs an integration plan.

Protect the accounts that make the acquisition worth the price paid

Identify the specific accounts inside each acquired company that justified the price you paid. Look past raw revenue size to find them, since the accounts a founder would fight hardest to keep are not always the biggest line items. Name an owner for each one on the day the deal closes. That owner is accountable for one thing: making sure that account’s relationship with the platform gets stronger through the transition. This is a different job than a sales quota and should be tracked separately from it.

| Dimension | Arithmetic-only platform | Relationship-integrated platform |

|---|---|---|

| Integration plan focus | Systems, reporting lines, cost savings | Named account owners, relationship continuity, systems second |

| What the deal math assumes | Revenue transfers automatically at close | Revenue transfer is treated as a risk with a plan to manage it |

| First 100 days | Org chart and back-office consolidation | Account-by-account relationship handoff, systems phased in after |

| Founder/key salesperson role after close | Assumed replaceable once the earnout ends | Actively transitioned, credibility handed off on purpose |

| What gets tracked | Cost savings, expense reduction | Cost savings and customer retention, tracked together |

| Typical failure mode | Quiet loss of accounts, discovered in year two or three | Rare, because the risk is visible and owned from day one |

Ready to grow?

Get a second opinion on where your current platform’s relationship risk actually sits.

How do you build a value creation plan for a buy and build platform?

A value creation plan for a buy and build platform should name the specific relationships and revenue sources the deal depends on, alongside the cost savings and growth targets. Most value creation plans are built around the standard math for growing profit: more revenue, fatter margins, a higher sale price down the road. A buy and build plan needs a fourth piece that the standard template leaves out: keeping relationships intact, with a named owner and a specific target for each acquired company.

Defined Term: Value creation plan.

The specific set of actions a private equity owner commits to during the time they hold a company, to grow what it’s worth, tied to named owners and measurable milestones.

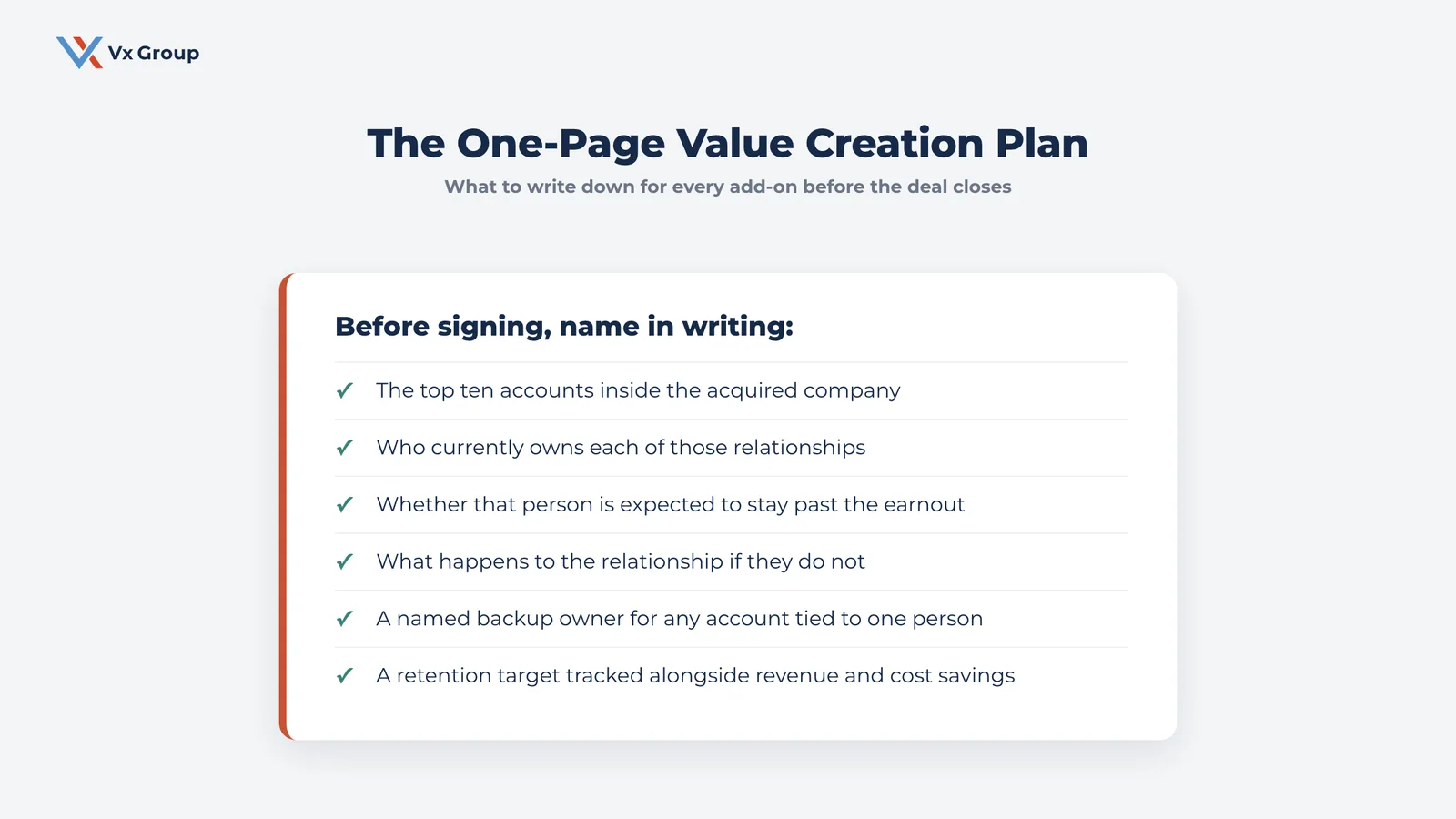

Write the one-page plan before the deal closes

Before signing, write one page per acquired company that names its top ten accounts, the person who currently owns each relationship, whether that person is expected to stay past the earnout, and what happens to the relationship if they do not. This single page belongs next to the financial model in the pre-deal check, built with the same rigor. If the team doing that check cannot produce it because the target’s account records are too thin, that thinness is itself a finding worth raising as a risk before the deal is priced.

Assign an owner for every key relationship on day one

Every account identified on that one-page plan gets a named human owner on the day the deal closes, announced internally and, where appropriate, to the customer directly. That owner reports on relationship health on the same schedule the CFO reports the numbers. Waiting until the ninety-day integration review to figure out who owns what account is how platforms lose the accounts that mattered most.

How do you integrate an add-on without breaking its customer relationships?

Integrate the systems and the reporting lines on a slower timeline than the sales team wants, and the relationships on a faster one than the integration playbook usually allows. Most buy and build integration plans move in the wrong order: consolidate the CRM, unify the invoicing, rebrand the correspondence, and only then get around to checking in on the accounts that made the acquisition worth the price. Flip that order. Confirm the top relationships are stable first. Change systems once trust in the new ownership is established.

Keep the acquired company’s point of contact visible through the transition

Whoever the customer has trusted for years, whether that is the founder, a longtime account manager, or a technical contact, stays the visible face of the relationship for a defined transition period. Set that period explicitly (ninety days, six months, whatever fits the account) and tell the customer directly what is changing and what they can count on staying the same.

Tell top accounts about the rebrand before they see it happen

If the acquired company’s name is disappearing into the platform brand, tell the top accounts before they read about it in an email footer. A short call or visit from the person they already trust, explaining exactly what is changing and what to expect next, prevents more lost business than any amount of marketing collateral explaining the new combined brand.

Field Notes:

One platform we worked with had bought four regional distributors inside eighteen months, each one profitable and well-regarded locally. The integration plan consolidated their CRMs and back-office systems in the first ninety days, which was the right call operationally. What it missed was that two of the four distributors had a single salesperson carrying relationships with accounts representing close to half of that distributor’s revenue. Neither salesperson was flagged as a retention risk in the pre-deal check, because the model only looked at how revenue broke down by account, with no view into which accounts depended on one relationship owner. One left within a year of his earnout ending. The accounts he owned did not immediately leave with him, but the platform’s leadership did not have a plan for introducing those accounts to a new contact, and eighteen months later, the platform had lost roughly a third of that book of business. The fix, once identified, was straightforward: a relationship map built for every acquired company before the next one closed, with named backup owners for every account tied to a single person.

What role should the operating partner play in a buy and build platform?

The operating partner in a private equity buy and build platform should own the regular check-in that surfaces relationship risk early, while the platform CEO and the acquired company’s own leadership own the relationships themselves. Operating partners typically meet with the companies they oversee on a monthly rhythm and can push, question, and escalate, but they do not run the business day to day. Their highest-value contribution in a buy and build platform is asking the questions that keep relationship risk visible at the ownership level.

Define what the operating partner owns versus what the acquired company’s CEO owns

Write this down explicitly rather than leaving it implied. The operating partner owns: setting the schedule for relationship health check-ins, asking the retention questions on every acquired company before it closes, and escalating when an account owner assignment has gone unfilled for more than a quarter. The acquired company’s CEO owns: the actual relationships, the account owner assignments, and the day-to-day judgment calls about how fast to move on rebranding, systems, or leadership changes inside their business.

Put relationship health on the same review schedule as the financials

Add a standing agenda item to the existing monthly or quarterly operating review: which accounts are flagged at risk, who owns them, and what changed since the last review. This takes fifteen minutes on an agenda that already exists. Most platforms never add it, which means relationship risk only becomes visible at the ownership level once it has already shown up as a revenue miss.

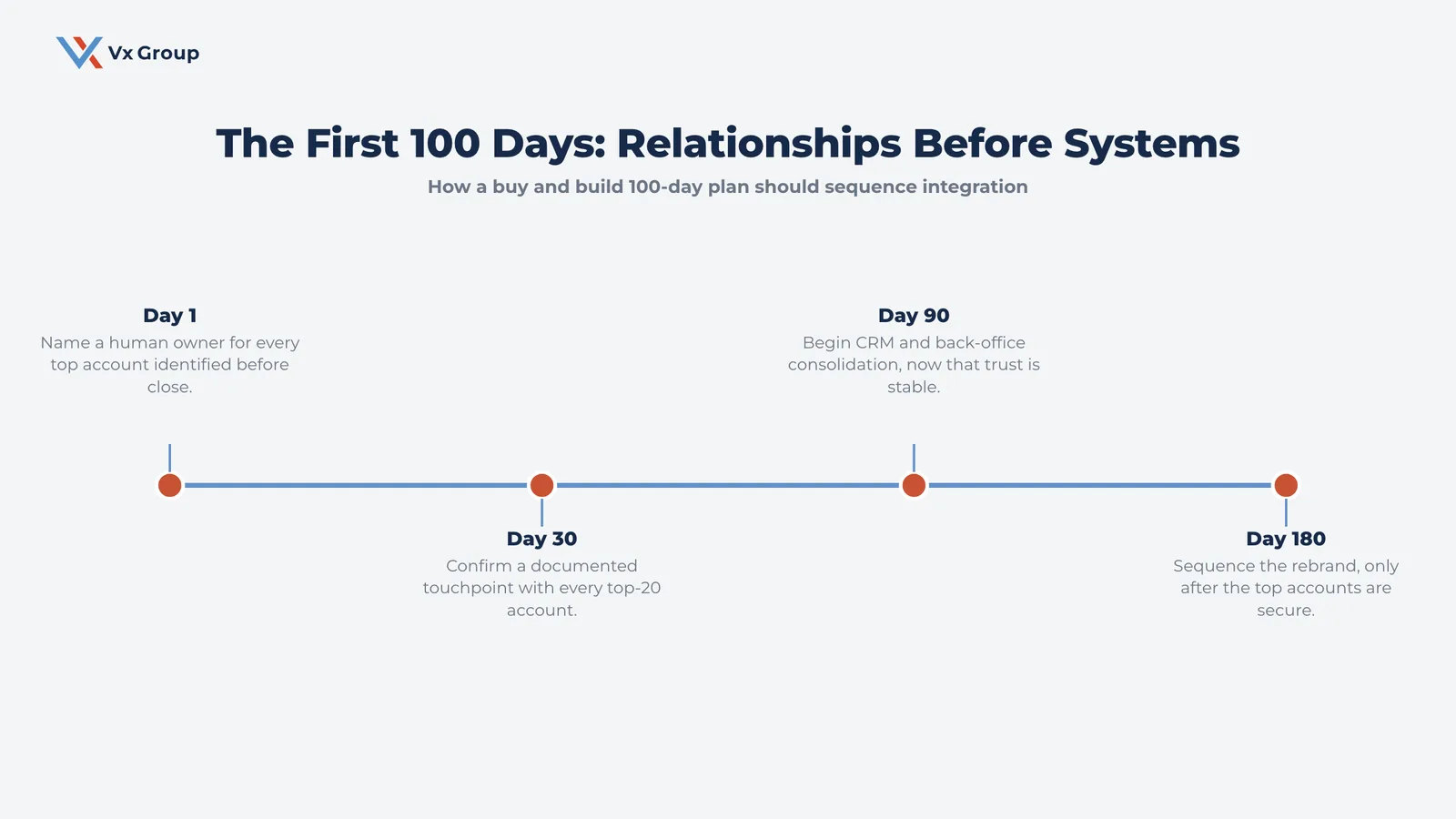

How do you run the first 100 days after buying an add-on company?

The first 100 days after a private equity acquisition should prioritize keeping accounts ahead of consolidating systems, because the accounts that leave in year two usually started checking out in month one. Most 100-day plans are written from an operations lens: org chart, IT systems, reporting structure, cost savings. A buy and build 100-day plan needs a parallel track focused entirely on the accounts identified in the value creation plan.

Name the account owner for every top relationship before day one

Do not wait until the deal closes to figure out who owns which account. Have this assigned and ready to communicate on day one, pulled directly from the one-page plan built before the deal closed. An account without a named owner in the first week of ownership is an account with no one accountable for whether it stays.

Keep the founder or key salesperson visible and engaged through the earnout

If the acquired company’s founder or top salesperson is staying through an earnout, give them a real, visible role in the first 100 days. Sidelining them while the platform’s team takes over reads to long-tenured customers as a sign something is wrong, whether or not it is.

Set the metric that tracks relationship health alongside cost savings

Add one number to the 100-day dashboard that a standard integration tracker leaves out: the percentage of top-20 accounts (across the whole acquired company, ranked by revenue) with a confirmed, documented touchpoint in the past 30 days. This is an early-warning number. Lost revenue shows up later, after the damage is already done. By the time it shows up, the relationship trouble happened months earlier.

Ready to grow?

See how this applies to the specific companies in your platform.

How do you measure whether a buy and build platform is actually creating value?

Measure a buy and build platform against customer retention and what the business is worth together, on the same scorecard, reviewed all the way through the hold period. Private equity value creation in relationship-driven B2B companies depends on durable customer relationships surviving ownership changes, and a buy and build platform stacks that risk across every company it acquires. A platform can hit its cost-saving targets and still be quietly losing the relationships that made the underlying companies worth buying.

Pair “what the business is worth” with customer retention on the same scorecard

Revenue can grow through price increases or new customer wins even while the original acquired relationships erode underneath it, masking the problem until it is expensive to fix. Track retention specifically for the accounts identified at acquisition, separate from total platform revenue, so the two trends cannot hide each other.

Track how much revenue rides on a handful of accounts

Track what percentage of each acquired company’s revenue sits with its top three accounts, and how that percentage changes year over year after the deal. A rising number here, even alongside overall revenue growth, usually means the smaller, more spread-out relationships are the ones eroding first, which is often the earliest sign of a weakening customer base. This is the same customer concentration risk that shapes value at any company a PE firm owns, acquired through a platform or not.

For a full view of what drives value in any company a PE firm owns beyond the buy and build model specifically, the same relationship-first logic applies to any company acquired standalone or folded into a platform.

Getting buy and build right

Buy and build strategies win or lose on the same factor in almost every case: whether the relationships underneath each acquisition survive the move to new ownership. The arithmetic behind combining companies and selling the package for more than the pieces cost is real and worth pursuing. It is also the easy half of the work. The harder half is naming an owner for every account that made the deal worth doing, keeping that owner visible through the earnout, and tracking relationship health with the same discipline applied to the cost-savings tracker.

Platforms that do this consistently outperform the ones that treat integration as a systems project, because they protect the exact revenue the purchase price was paid for in the first place.

Ready to grow?

Get a second opinion on where your platform’s relationship risk actually sits before the next deal closes.