Portfolio Company Value Creation: What Actually Drives It

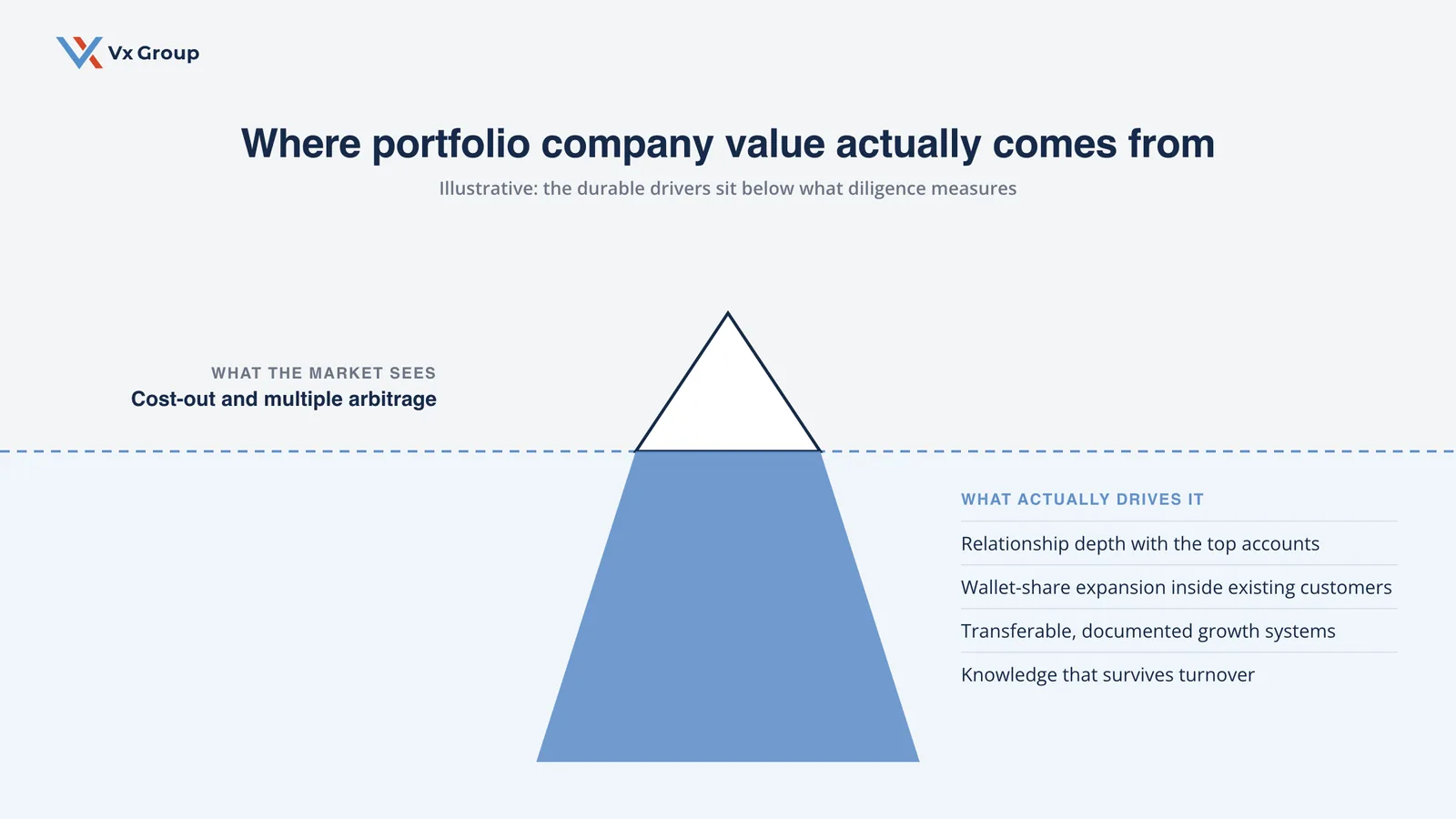

Portfolio company value creation is the work of turning an acquired business into a more valuable one over the hold period. Most of that value is created two ways: cutting cost to lift margin, and buying or selling at a better multiple. The durable gains come from a third place that rarely shows up in the model, which is the depth and transferability of the company’s customer relationships.

TL;DR

- Portfolio company value creation means increasing the worth of an acquired company between entry and exit, usually through margin improvement, multiple expansion, and revenue growth.

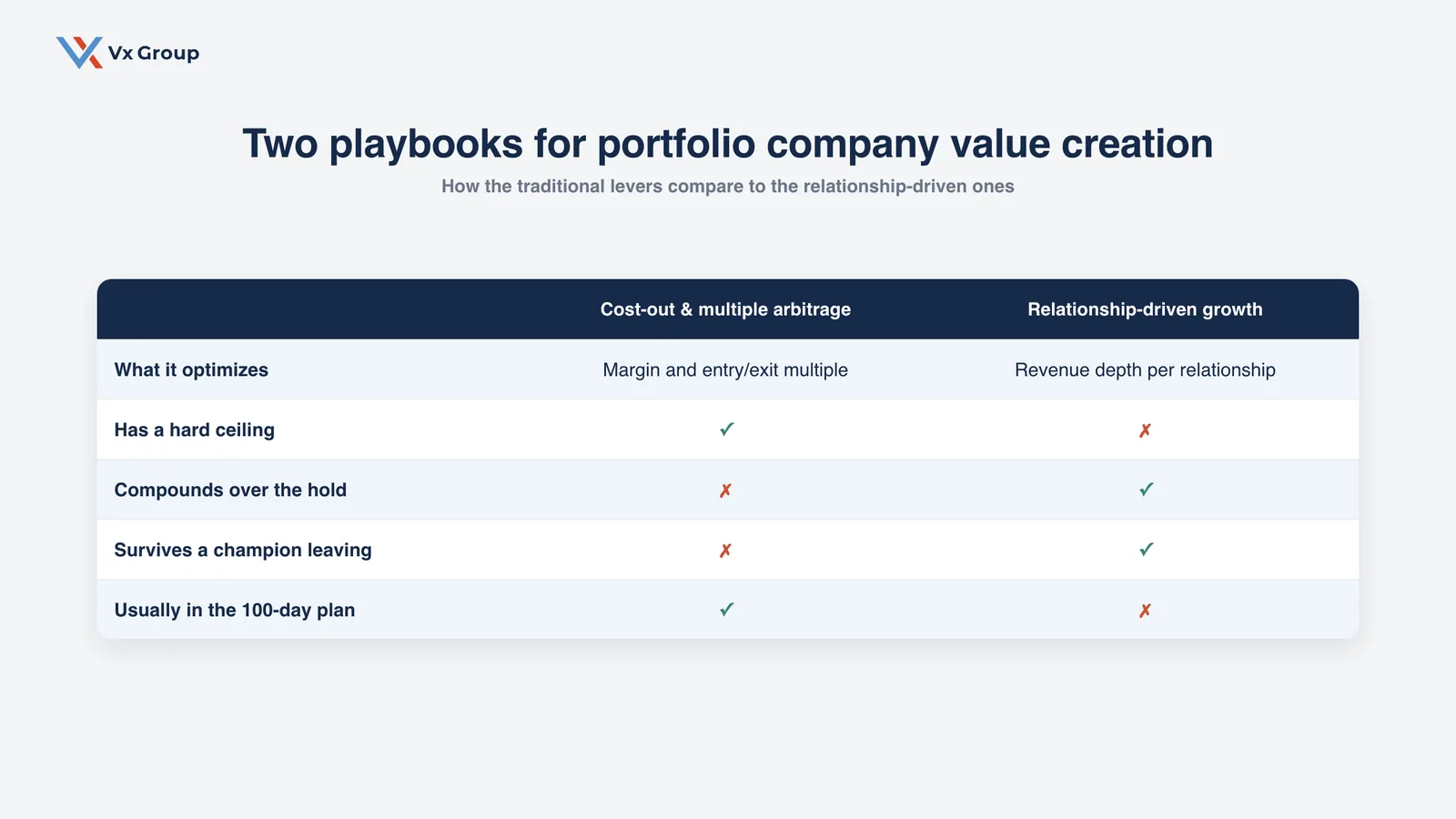

- Cost-out and multiple arbitrage work, and they have a floor. You can only take so much cost out before you start cutting into the business that produced the returns.

- In relationship-driven B2B companies, the value that compounds lives in three places: relationship depth with the top accounts, wallet-share expansion inside existing customers, and growth systems that transfer to new owners.

- Diligence and the 100-day plan almost always measure the financial layers and skip the relationship layer, which is where the real risk and the real upside sit.

- The fastest path to a stronger exit is usually protecting and expanding the relationships you already own before spending to replace them.

What is portfolio company value creation?

Portfolio company value creation is everything a sponsor does to make an acquired company worth more at exit than it was at entry. In practice it runs on three engines: improving margin, growing revenue, and expanding the multiple the market will pay. The first two change the company. The third changes how the company is priced.

Defined Term: Portfolio company value creation

The set of operational, commercial, and financial moves a private equity or family office owner makes to raise a portfolio company’s enterprise value over the hold period, measured as the gap between entry and exit value.

I spend a lot of time with sponsors and operators in relationship-driven B2B companies, the kind with long sales cycles, a handful of accounts that matter enormously, and revenue that has been built over decades. In those businesses, the standard value-creation playbook gets you part of the way. The part it misses is usually the part that determines whether the next owner pays a premium or a discount.

How to read your own value-creation mix

Look at your last few value-creation plans and sort the initiatives into three buckets: margin, multiple, and revenue. Most relationship-driven portfolio companies find that ninety percent of the plan lives in margin and multiple, and almost nothing is aimed at deepening the customer relationships that produce the revenue. That imbalance is the opportunity. It tells you exactly where the underused lever is sitting.

What actually drives portfolio company value creation in relationship-driven companies?

In relationship-driven B2B companies, three drivers create value that holds up at exit. They all sit in the commercial layer of the business, and they all compound the longer you own the company.

- Relationship depth with the top accounts. The lifetime value concentrated in a company’s ten largest relationships often exceeds the entire pipeline of new prospects.

- Wallet-share expansion inside existing customers. Most acquired companies are selling a fraction of what their best customers actually buy in their category.

- Transferable growth systems. When growth lives in one founder’s head or one rainmaker’s relationships, a buyer discounts for key-person risk.

Defined Term: Wallet-share expansion

Growing revenue by capturing a larger share of an existing customer’s total spend in your category, rather than acquiring new customers.

These three are not soft. They show up directly in revenue quality, customer concentration risk, and the credibility of the growth story you tell at exit.

Deepen the relationships that carry the company

Start by finding out who actually owns each of your largest relationships, then make sure more than one person does. When a single rep holds the entire connection to a top account, you do not have a relationship, you have a liability with good revenue attached. Add an executive sponsor to each key account, get a second relationship started inside the customer, and you raise revenue and lower risk in the same move.

Expand wallet share before chasing new logos

Map what each of your top customers buys from you against what they buy in your category overall. The gap is your cheapest growth. Expanding into an adjacent product line, a second site, or another division of a customer who already trusts you costs far less than winning a stranger, and it lands faster. A lot of acquired companies have been order-taking from their best accounts for years without ever asking for the rest of the budget.

Turn the growth motion into transferable systems

Sit with your best two or three commercial people and document how they actually win and keep business. Write down how they open a relationship, how they expand it, how they handle a renewal, and what they do when an account goes quiet. That documentation is what converts founder-dependent growth into a system the next owner can run. Buyers pay for predictability, and predictability is just a documented motion that works.

Ready to grow?

If your portfolio company’s growth still lives in a few people’s heads, that is exactly the kind of motion we help install as a system.

Why do cost-out and multiple arbitrage hit a ceiling?

Cost-out and multiple arbitrage hit a ceiling because both are finite. There is a fixed amount of cost you can responsibly remove from a business, and once you have removed it, the lever is spent. Multiple expansion depends heavily on market timing and the story you can tell, which means a lot of it is outside your control.

Operational efficiency has a floor. You reach a point where the next dollar of cost you cut starts damaging the thing that made the company worth buying: the service quality, the responsiveness, the people who hold the customer relationships. A lot of operators know exactly where that floor is and stop short of it. Some push past it under pressure and quietly erode the franchise.

Relationship-driven growth works the other way. Every relationship you deepen and every system you document makes the next quarter a little easier than the last. That is the difference between a lever you pull once and an engine that keeps running.

How to tell when you are near the cost floor

Watch for three signals. Response times to your best customers start slipping. The people who hold the key relationships begin updating their resumes. And the same accounts that drove the thesis start mentioning a competitor by name. Any one of those means the next cut will come out of the franchise, not the fat. When you see them, stop cutting and start investing in the relationship layer, because that is where the remaining value is.

Where does durable value creation actually happen in the business?

Durable value creation happens in the relationship layer, which is the part of the business most commercial due diligence and most 100-day plans never touch. Diligence is very good at the financials, the contracts, the customer concentration numbers, and the org chart. It is far less good at answering a simpler question: if the wrong person left next month, how much revenue would walk out with them?

That question matters because in these companies, a single retirement or resignation can dissolve millions in relationship value overnight. The knowledge of how to serve a key account, the trust built over fifteen years, the reason the customer keeps coming back, often live entirely in one person. Systems make that knowledge repeatable and protect it. They do not replace the human relationships. They make sure the relationships survive a transition, including the ownership transition you are planning for at exit.

This is the same idea behind treating customer relationships as the most underrated asset on a B2B balance sheet. The asset is real, it produces most of the cash flow, and almost nobody manages it like an asset.

For the broader frame on how sponsors build durable value in these businesses, our pillar on how private equity creates value in relationship-driven B2B companies walks through the full model.

What to add to your diligence and 100-day plan

Add a relationship map to diligence: the top accounts, who owns each one internally, how long that person has held it, and what happens to the revenue if they leave. In the 100-day plan, name an owner for each key relationship, set a baseline for relationship health, and put wallet-share expansion targets next to the cost targets. None of this is expensive. It just requires looking at the layer the standard checklist skips.

How does relationship-driven growth compound over the hold period?

Relationship-driven growth compounds because each of its inputs feeds the next. A deeper relationship with a top account opens the door to more of that customer’s spend. Capturing more of their spend gives you more reasons to stay close, which deepens the relationship again. Document how your best people do this, and the pattern repeats across the customer base instead of staying trapped with one rep.

Over a typical hold, that compounding shows up as three things a buyer is willing to pay for: revenue that is growing inside the existing base, customer concentration risk that is going down because no single person owns the whole relationship, and a growth motion the next owner can run without the current founder in the room. Those are the exact attributes that move a multiple, and you build them by doing the relationship work, not by waiting for the market to cooperate.

How to start the flywheel in the first 90 days

Pick your three largest accounts and run the loop on them first. Get a second relationship going inside each one, ask for a piece of spend you are not currently winning, and write down what worked. Three accounts is enough to prove the motion and build the template you will roll out to the rest of the base. You do not need a transformation program to start. You need three relationships and the discipline to document what happens.

How do you build a relationship-driven value creation plan?

You build a relationship-driven value creation plan by treating your existing relationships as the asset they are: name owners, measure health, set a contact rhythm, and document the motion so it survives turnover. None of these steps requires new headcount or a big technology spend. They require deciding that the relationship layer gets managed with the same rigor as the P&L.

Name a real owner for every key account

Assign one accountable owner to each top relationship, and make sure it is not the same person chasing every new deal, because urgent always beats important. Ownership means someone is responsible for the health of the relationship, not just the next order. Write it down so it survives the next reorg.

Track relationship health like you track pipeline

Build a simple scorecard for your top accounts: when a real conversation last happened, whether spend is growing or flat, how many people inside the customer you have a relationship with, and whether you would hear about an RFP before it published. Most companies report in detail on open deals and almost nothing on the accounts they are trying to keep. Flip that.

Build an executive contact rhythm that does not wait for problems

Put a documented cadence in place that brings senior people into key accounts between problems, not just when something breaks. A standing quarterly conversation at the executive level does two things: it surfaces expansion opportunities early, and it makes sure the relationship does not live entirely with one rep who could leave.

Document how your best people create growth

Capture the actual plays your top performers run, then make them the standard. This is the step that turns a personality-dependent business into a transferable one. It is also the step that shows a buyer the growth will continue after the current team is gone, which is what they are really paying for at exit.

The bottom line for sponsors and operators

The standard value-creation model is not wrong. Margin, revenue, and multiple are real, and you should work all three. The point is that in relationship-driven B2B companies, the cost-out and arbitrage levers run out, and the relationship layer is where the value keeps building and where the biggest risk hides in plain sight.

If you are holding one of these companies, the highest-return work is often the least glamorous: name a real owner for every key account, track relationship health as closely as you track the pipeline, expand inside the customers you already have, and document how your best people actually create growth so it survives the next transition.

Do you know who owns each of your portfolio company’s ten most important relationships? And if that person left tomorrow, do you know how much of the exit story would leave with them?

Ready to grow?

If you want a clear-eyed read on where the durable value in your portfolio companies actually sits.