What a Private Equity Investment Thesis Really Measures

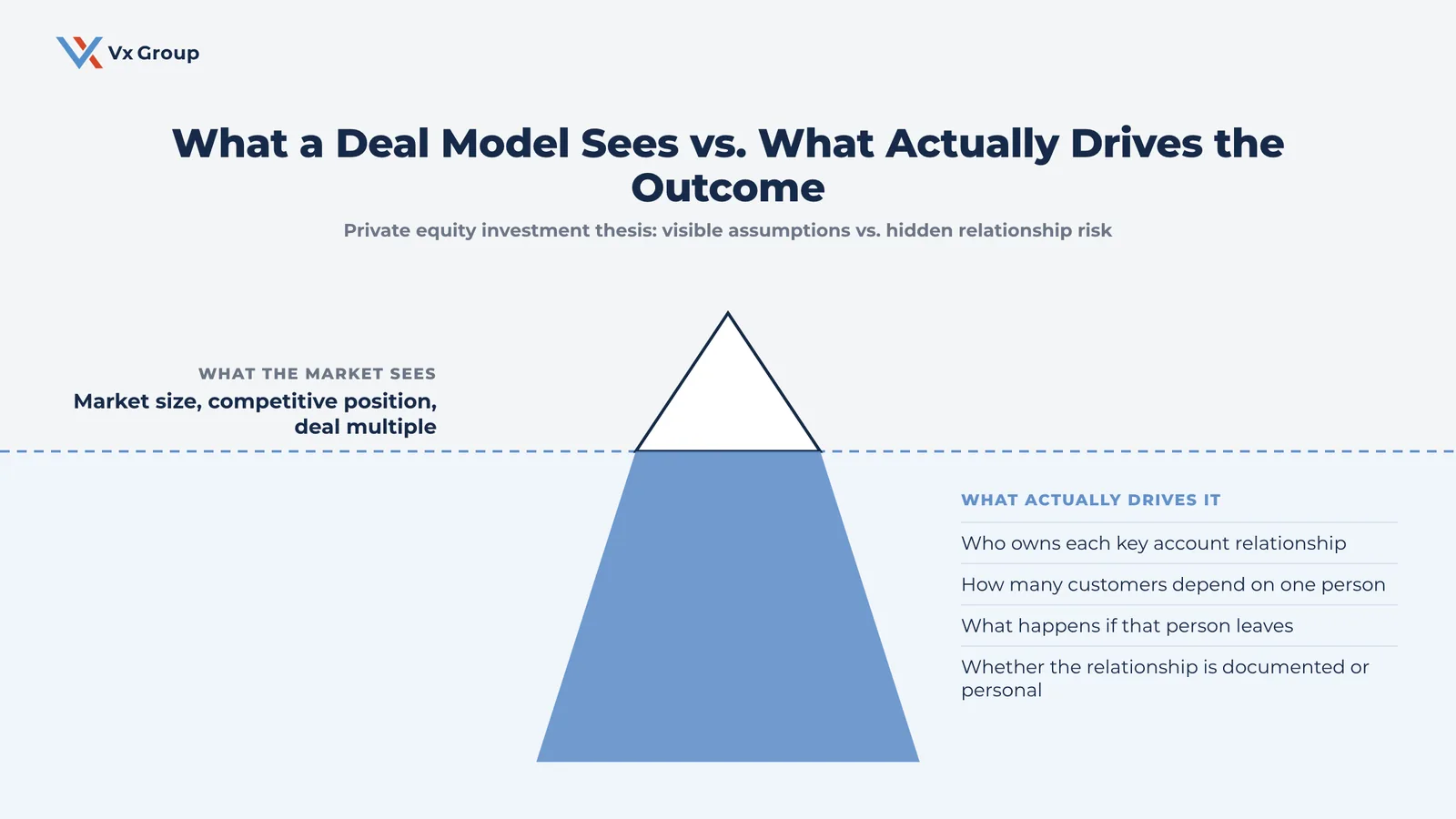

A private equity investment thesis measures more than market size, competitive position, and the expected multiple. It measures whether the growth assumptions inside the deal model survive a change of ownership, specifically whether the customer relationships that produced the target’s revenue transfer to the new owner or stay with the people who built them.

TL;DR

- A thesis usually documents market, moat, and multiple. It rarely tests whether customer relationships survive the sale.

- In relationship-driven B2B companies, revenue concentrates with specific people. The logo on the door often has little to do with it.

- Commercial due diligence checks whether revenue is real, but it rarely checks whether that revenue survives new ownership.

- A growth-ready thesis names who owns each key relationship, how it was built, and what happens if that person leaves.

- The gap between a thesis on paper and a thesis that holds up after close is almost always relationship risk nobody underwrote.

Every investment committee memo tells roughly the same story. The market is big enough. The company holds a real position in it. The math works at the multiple on the table. That story gets tested hard before signing. Market sizing gets checked against third-party data. The competitive position gets pressure tested against named rivals. The model gets stressed against a downside case.

A lot of theses stop there, and a lot of them get quietly rewritten in the first year of ownership. The revenue itself moved. A regional sales rep left eighteen months after close and took a customer with him. A distributor relationship that looked contractual on paper actually ran through one aging owner-operator who retired the year after the deal. The thesis had priced the growth. Nobody had priced who actually owned the relationships that growth depended on.

What does a private equity investment thesis actually document?

A private equity investment thesis documents three things: the size and durability of the market, the company’s competitive position inside it, and the return the deal produces at a given multiple and hold period. It is the argument for why capital returns, built to survive scrutiny from an investment committee before the wire goes out.

Size the market with named, checkable data

Market sizing should come from sources a skeptical partner can verify independently. A chart pulled from a banker’s deck rarely survives that kind of scrutiny. A thesis built on an unsourced market-size number is a thesis nobody has actually tested. Name the source, the year, and the method every time a market figure appears in the memo.

Name the moat honestly

The moat is whatever keeps a competitor from taking the business at will. Management decks tend to reach for brand strength, product quality, or switching cost as the answer. Those things matter, but in relationship-driven B2B companies the more honest answer is often “the relationships between our sales team and the twenty accounts that produce sixty percent of revenue.” That is a real moat. It is also a fragile one when it depends on individual people instead of an institutional system the buyer will own after close. Write down the moat that actually holds the business together.

Model the return math against a downside growth case

The return math should hold up when growth comes in below plan, and it should also hold up when it hits the base case used to justify the price. A thesis that only works at management’s projected growth rate is really a bet on management’s forecast. The underlying business may carry a much wider range of outcomes than that single number suggests. Build the downside case with the relationship risk already baked in: give the specific at-risk accounts a haircut sized to their actual risk, so the committee sees a return that reflects what actually happens if a key account owner leaves in year one.

Where do most investment theses break down after close?

Most investment theses break down after close because they assumed the revenue transfers with the sale. In relationship-driven businesses, a meaningful share of that revenue actually belongs to the person who built the relationship, and the company on the cap table owns the contract while a specific salesperson or account manager often owns the trust that keeps the customer buying. The deal model usually treats every dollar of trailing revenue as equally durable, an assumption that rarely holds up once ownership changes.

Defined Term: Field Notes

A platform company we worked with had built its thesis on a distribution business generating close to $8 million a year through eleven regional partners. Diligence confirmed contracts, tenure, and payment history for every one of them. What diligence did not surface was that four of those eleven relationships ran through a single VP of sales who had personally recruited each partner over fifteen years. He left fourteen months after close. Two of the four partners followed him within the year. The thesis had priced that eight million in revenue as a known quantity. For four of those relationships, it was closer to a personal book of business the deal happened to be renting.

What is the customer relationship blind spot in an investment thesis?

The customer relationship blind spot is the assumption, usually unstated, that the revenue attached to a target company belongs to the company itself. In practice, the individual people who built and maintain each account frequently hold a large share of that revenue in their own personal relationships.

Defined Term: Relationship durability risk

the portion of a target’s revenue that depends on a specific individual’s personal relationship with a customer or partner, revenue with no documented, transferable system behind it that the buyer can actually own after close.

This risk concentrates hardest in exactly the companies private equity finds most attractive: legacy manufacturers, distributors, and industrial services businesses with decades of tenure, loyal accounts, and thin systems documentation. The same twenty-year relationships that make the revenue look stable are frequently held together by two or three people whose departure the deal model never modeled.

Revenue concentration by account name looks fine on paper in many of these deals. The top twenty accounts are diversified, none over ten percent of revenue, nothing that would trip a diligence flag. Concentration by relationship owner tells a different story. If three of the top twenty accounts all answer to the same regional manager, the real concentration risk is three times higher than the account-level number suggests, and the deal model has no line item for it.

Defined Term: Relationship concentration

the share of a target’s revenue that sits with accounts controlled by the same individual relationship owner. It is distinct from customer concentration, which only measures revenue share by account name, and it is usually invisible in a standard diligence report.

Why does this risk hit relationship-driven B2B harder than other deal types?

This risk hits relationship-driven B2B harder than other deal types because revenue in these businesses concentrates in a small number of large, personal relationships. Subscription and other high-volume businesses spread revenue across thousands of small, self-service transactions where no single relationship carries much weight.

A subscription software business built on thousands of individual accounts rarely has this problem. No single salesperson’s departure moves the revenue line in a way that threatens the thesis, because no single person owns enough of the relationship to matter. A legacy manufacturer, distributor, or industrial services business built over twenty or thirty years is the opposite case.

A handful of long-tenured people, often the same people who founded the sales function, personally hold the trust behind a large share of total revenue. That is exactly the kind of business private equity finds attractive: stable, cash generative, defensible. It is also exactly the kind of business where the growth playbook has to differ from the one built for high-velocity, product-led deals.

Borrowing diligence and value-creation methods built for a different kind of company is a common and avoidable mistake. The checklist that works for a horizontal SaaS platform will miss the relationship concentration sitting inside a distribution business, because the checklist was never built to look for it. Diligence and the post-close plan both need to be built for the actual business in front of them, with its own concentration patterns and its own risks.

How do you test whether customer relationships transfer with a deal?

You test relationship transfer by mapping revenue to the person who owns each account, then scoring the accounts that carry the most concentrated risk before the deal closes.

Map revenue by relationship owner

Pull the target’s top twenty accounts by revenue and answer a simple question for each one: who, specifically, is the reason this customer buys from this company. Not the sales territory. Not the CRM record. The actual person with the actual relationship. Group the accounts by owner and the real concentration risk usually looks worse than the account list alone suggests.

Get direct access to key accounts before signing

A seller who resists letting the buyer’s team speak with key customers before close is often protecting exactly the risk this thesis needs to price. Even short, structured conversations with the ten or fifteen largest accounts surface whether a relationship is institutional or personal far faster than any contract review. Ask each customer a version of the same question: if the person you deal with today left the company, would you still buy at the same volume next year? The hesitation in the answer is often more informative than the words.

Score each key account for durability

Rate the top twenty accounts on three factors: how many people at the target touch the relationship, whether the customer has ever dealt directly with ownership or only with one rep, and how the account would likely respond to that rep’s departure. Accounts with a single point of contact and no documented history score as high risk regardless of tenure or contract length.

Price the risk into the model

Once the scoring is done, run the growth model twice: once as built, and once with the flagged high-risk accounts held flat or removed entirely. The gap between those two outcomes is the real size of the risk the thesis is carrying. Accounts that move the return meaningfully in that second run need a specific haircut in the model or a specific line item in the value creation plan. A footnote that quietly disappears once the deal signs does not count as pricing the risk.

What should a growth-ready investment thesis include?

A growth-ready investment thesis includes everything a traditional thesis includes, plus a documented answer to who owns each key relationship and what happens to revenue if that person leaves. That single addition changes how a deal gets underwritten and how it gets managed after close.

This is the difference between a thesis that predicts a return and a thesis that protects one. How private equity creates value in relationship-driven B2B companies comes down to whether the operating team can see this risk clearly enough to manage it. Most of the businesses private equity buys in this category are good businesses with real customers and real demand. The risk sits in losing what made them good during the transition of ownership.

None of this requires a heavier diligence process across the board. It requires pointing the existing process at a question it was not built to ask. The market analysis, the moat analysis, and the multiple math stay exactly as rigorous as they already are. What changes is a single added lens: for every dollar of revenue in the model, who specifically is the reason that dollar shows up, and does the answer survive a change in ownership.

How does this change commercial due diligence and the first months after close?

This changes commercial due diligence by adding a relationship-durability layer to the standard revenue-quality review, and it changes the first months after close by making relationship transition an explicit workstream with a named owner, alongside the usual financial integration work.

Commercial due diligence traditionally measures whether reported revenue is real: contracts, churn history, pricing, and customer concentration by dollar amount. It rarely measures concentration by relationship owner, which is a different and often larger risk in relationship-driven businesses. Adding that layer typically costs a few extra weeks of diligence work. Compared to discovering the risk fourteen months after the wire clears, that cost is small.

Once the deal closes, the accounts flagged as high risk need a named plan in the first few months of ownership. A line item that waits for the annual review comes too late to matter.

In practice that means the new ownership group meeting directly with the highest-risk accounts early, documenting what the departing or at-risk relationship owner actually does day to day, and building the systems that make the relationship transferable going forward. This is the same discipline behind strong portfolio company value creation work broadly.

Documented systems are what let growth survive a management change. When growth depends on one person’s rolodex, the thesis is carrying an undisclosed bet that surfaces the day that person walks out the door.

What should the investment committee ask before approving the deal?

The investment committee should ask who owns each of the top twenty accounts, how that ownership was verified, and what the growth model assumes happens if any of those relationship owners leaves within the first two years. These three questions surface the relationship durability risk before the deal is priced, when the answer still has leverage over the terms.

Asking these questions before signing matters more than asking them after. Before signing, a real answer can change the price, the structure, or the reps and warranties in the purchase agreement. After signing, the same answer is just a problem the new owner inherits with no recourse. The sequence is the entire point. A committee that raises relationship durability during the negotiation has a lever it loses the moment the deal closes.

A short table is often the clearest way to bring this to an investment committee:

- Account concentration by dollar amount: already standard in most memos, and necessary, but not sufficient on its own.

- Account concentration by relationship owner: rarely in the memo, and frequently more revealing than the dollar figure alone.

- Owner tenure and succession plan: whether a documented successor exists for each high-risk relationship, or whether the knowledge lives with one person and nowhere else.

- Post-close relationship plan: the specific first-ninety-day actions assigned to a named person for each account scored as high risk.

A committee that can answer all four questions before signing has priced a risk that most competing bidders never modeled. That is a real edge in a competitive process. In a crowded auction, most bidders show up with the same market and moat talking points pulled from the same data room. A bidder who can speak specifically to relationship durability often stands out to a seller who already knows, quietly, exactly where the business is fragile.

Conclusion

An investment thesis is supposed to be the argument for why a deal returns capital. In relationship-driven B2B companies, that argument is incomplete until it accounts for who actually owns the relationships behind the revenue. Market sizing, competitive position, and multiple math get real scrutiny before every deal. Relationship durability, just as often, gets none.

The fix is not complicated. It is a handful of extra questions during diligence, a different way of grouping the top accounts, and a named plan for the relationships that score as fragile. None of it requires walking away from a good business. Most of the businesses that carry this risk are still good businesses worth buying. The fix simply means buying them with an accurate picture of where the growth actually comes from, instead of finding out the hard way in year two. The theses that hold up after close are the ones that priced this risk before signing.

Ready to grow?

See how a relationship-durability review would change the growth assumptions in your next deal.

Subscribe to Insights → Get the next private equity growth field note the week it publishes.