How Operating Partners Can Drive Growth in Private Equity

An operating partner in private equity is the person accountable for turning a portfolio company’s potential into realized value. The role exists to own growth itself, well beyond monitoring and reporting. The highest-return move an operating partner can make is installing a growth system the leadership team owns and runs, so progress continues between board meetings and survives after the firm exits.

TL;DR

- An operating partner is a senior operator inside a PE firm who is accountable for portfolio company performance, most often revenue growth and margin expansion.

- Most value-creation plans stall because the operating partner defaults to oversight and reporting instead of building something the company can run on its own.

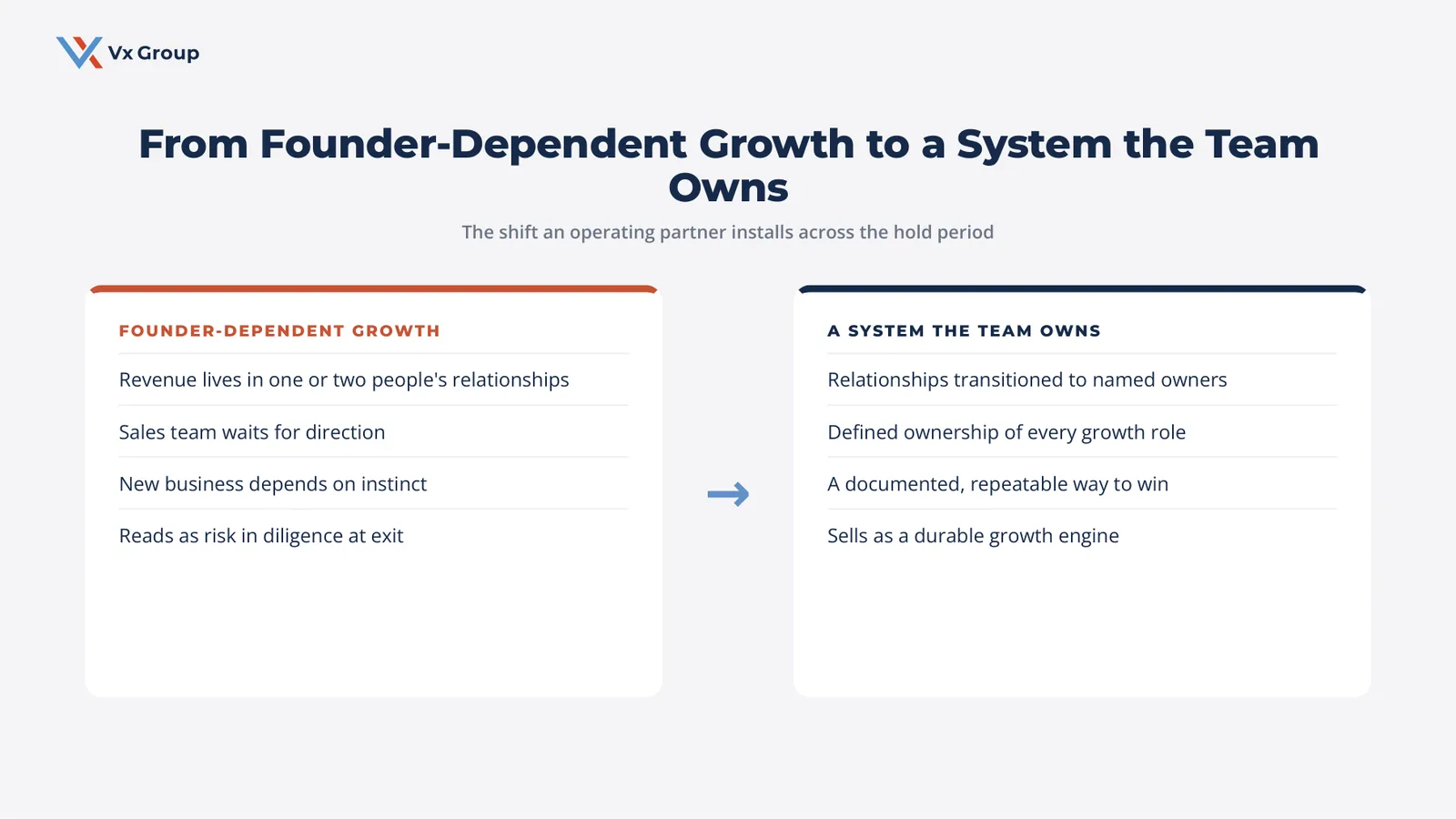

- The companies that compound value have a documented growth system: a clear picture of where they win, defined ownership, priority markets, and a follow-up rhythm that does not depend on the founder.

- The operating partner’s job is to install that system in the first 90 to 180 days, then coach the leadership team to own it.

- Growth that depends on the operating partner’s presence is a liability at exit. Growth that lives in a system the team owns is an asset a buyer will pay for.

What does an operating partner in private equity actually do?

An operating partner works inside a private equity firm and is responsible for improving the performance of portfolio companies after the deal closes. Where a deal partner sources and structures the investment, the operating partner is measured on what happens next: revenue growth, margin expansion, operational improvement, and a cleaner, more valuable business at exit.

The title sits apart from the investment team for a reason. Deal professionals are wired to evaluate and acquire. Operating partners are wired to build. Most come from 15 to 25 years of running businesses as a CEO, COO, or functional leader, and they carry that scar tissue into the portfolio. They have closed plants, rebuilt sales teams, fixed broken pricing, and lived through the quarters where a plan looked good on a slide and fell apart in execution.

In practice, an operating partner splits time across three jobs. Diligence support before a deal, where they pressure-test the growth thesis. Active engagement after close, where they work alongside the leadership team to execute the value-creation plan. And portfolio-wide pattern work, where they carry what works at one company to the others.

Defined term: Value-creation plan

The documented thesis for how a portfolio company will be worth more at exit than at acquisition. It names the specific moves, like entering a new market, fixing pricing, or professionalizing the sales function, and assigns ownership and timing to each. A value-creation plan that lives only in the firm’s files is a forecast. One installed inside the company is a system.

How is an operating partner different from a management consultant?

An operating partner carries accountability for the outcome and shares the firm’s economic stake in it. A consultant delivers a recommendation and moves on. That difference changes everything about how the work gets done.

A consultant is hired for a defined scope, produces analysis, and leaves the implementation to the client. The relationship ends when the deliverable lands. An operating partner stays through the hold period, sits close to the leadership team, and is judged on whether the plan actually produces the return. Their compensation is often tied to the fund’s carry, so a portfolio company that underperforms costs them personally.

That accountability is also the trap. Because operating partners are measured on results and have limited time across a portfolio of six, eight, or ten companies, the pull toward oversight is strong. Reviewing dashboards and running monthly check-ins feels like progress. It produces reports. What it rarely produces is a company that grows faster on its own.

Where do most operating partners get stuck?

Most operating partners get stuck managing the portfolio company instead of building its capacity to grow without them. They inherit a business with no documented growth system, so they fill the gap with their own attention, and that attention becomes the system.

This is the pattern worth naming. A firm acquires a strong lower-middle-market company, often a founder-led business that grew on reputation and relationships. The numbers are solid. The customer base is loyal. The value-creation plan calls for accelerated growth. The operating partner arrives, runs diligence on what is broken, and starts working the problems directly.

Six months in, growth has improved, but only where the operating partner is personally involved. The sales team still waits for direction. The founder still owns the most important relationships. New customer acquisition still depends on a few people’s instincts. The operating partner has become the growth engine, which means the firm now owns a business that runs on a resource it cannot leave in place.

Defined term: Founder-dependent growth

A growth model where revenue depends on the relationships, instinct, and presence of one or two people, usually the founder. It looks like strength while those people are engaged. At exit it reads as risk, because a buyer is paying for a business that may not function once the key people leave.

The same trap shows up at the portfolio level. An operating partner spread across eight companies cannot personally run growth at any of them. The ones that improve and hold their gains are the ones where a system got installed. The ones that backslide the moment attention moves elsewhere never had a system at all.

Why does installing a growth system beat running growth directly?

A growth system produces results whether or not the operating partner is in the room, which is the only kind of result that holds up at exit. Running growth directly produces results that disappear when attention moves to the next company or the next fire.

Three reasons make the system approach the higher-return choice for anyone responsible for portfolio growth.

Better reach across the portfolio

One operating partner cannot be the growth function for ten companies. A documented system that each leadership team owns scales in a way that personal involvement never will. The operating partner’s time shifts from doing the work to installing the capability, then coaching it.

Increased durability through the hold

PE hold periods run three to seven years, and leadership changes, market shifts, and team turnover happen inside that window. A company whose growth lives in one person’s head loses momentum every time that person changes roles. A company with a documented system absorbs the change and keeps moving.

Higher valuation at exit

A buyer pays more for a business that has a repeatable way of acquiring and expanding customers than for one that has been growing on the operating partner’s borrowed effort. The system itself is part of what gets sold. Quality of earnings improves when the growth behind those earnings is structural rather than heroic.

Ready to grow?

Install a repeatable growth system in your portfolio companies, instead of running growth yourself deal by deal.

What does a growth system for a portfolio company include?

A growth system has five working parts: a clear picture of where the company already wins, defined ownership of growth, a focused set of priority markets, a profile of the ideal customer, and a follow-up rhythm that runs without the founder. Each part is documented, owned by someone on the leadership team, and measurable.

This is the documented plan an operating partner can install. Work through it in order, because each part depends on the one before it.

Defined term: Growth system

A documented, owned, and repeatable way a company acquires and expands customer relationships. It replaces instinct and individual effort with a structure the leadership team runs. The test of a real growth system: if the founder took a month off, would new business still progress? If yes, the system exists. If no, the founder is the system.

Part 1: Build a clear picture of where the company already wins

Start by mapping where revenue actually comes from and why the best customers chose this company. Most lower-middle-market businesses have never documented this, so growth decisions get made on instinct instead of evidence.

Rank the customer base by relationship quality and lifetime value rather than current-year revenue alone. The largest account is not always the best one. Look for the customers who stay, expand, refer, and pay on time. Then find the pattern they share: industry, size, the problem they hired the company to solve, the decision-maker who signed off, and how the relationship started. That pattern is the company’s real growth thesis, and it is usually more specific than anyone expected.

This step alone resets a lot of value-creation plans. A firm that assumed the path was geographic expansion often finds the real opportunity is deeper penetration of one industry where the company quietly dominates.

Part 2: Define who owns growth

Name the person accountable for each part of growth: new customer acquisition, existing account expansion, and the marketing that supports both. In founder-led companies these roles usually live with the founder by default, which is the bottleneck the value-creation plan needs to remove.

Growth stalls when everyone is responsible, which means no one is. Write down who owns the target list, who owns outreach, who owns the proposal, and who owns the follow-up after a deal closes. Where a role has no owner, that gap is the first thing the operating partner should fix, often by hiring or promoting before doing anything else.

The goal is a growth function that does not route every decision through the founder. That is what makes the company sellable as a growth story rather than a personality.

Part 3: Choose priority markets

Focus the company’s effort on the two or three markets where it has the clearest right to win, and say no to the rest for now. Spreading a lean team across every possible market is the fastest way to produce activity without results.

Use the pattern from Part 1. The priority markets are the ones that look like the best existing customers: same industry, same problem, same buying behavior. Concentrating effort there raises win rates, shortens sales cycles, and makes the limited time of a small commercial team count. An operating partner who narrows focus here usually sees pipeline quality improve within a quarter.

Part 4: Document the ideal customer profile

Write a specific, evidence-based profile of the customer worth pursuing, built from the company’s actual best relationships rather than a wish list. A profile that says “manufacturers with revenue over 10 million” is too broad to be useful. A profile that names the industry, the operational trigger that creates need, the title of the buyer, and the reason this company wins that buyer is a tool the whole team can use.

This profile is what turns scattered prospecting into focused effort. It tells the sales team who to call, the marketing team who to speak to, and the leadership team which opportunities to walk away from. Without it, a growth plan is a volume play, and volume plays are exactly the wrong move for a relationship-driven business with long sales cycles.

Part 5: Install a follow-up rhythm the founder does not run

Build a documented cadence for staying in front of priority relationships, and assign it to someone other than the founder. Most lower-middle-market companies lose deals not because they were beaten but because they went quiet. The relationship cooled while everyone was busy with delivery.

A simple, written rhythm fixes this. Define how often the team touches active prospects, what the touch consists of, and who is responsible. Capture it in the CRM so it survives turnover and vacations. This is the part of the system that most directly protects revenue, because it keeps the company present in relationships that take months or years to convert.

Field Notes: A founder-led manufacturer after acquisition

A PE firm acquires a precision components manufacturer doing 28 million in revenue. The founder owns the top ten relationships and personally closes every deal over a certain size. The value-creation plan calls for 40 percent revenue growth over the hold.

The operating partner’s first instinct is to add a VP of Sales and push for more activity. That would have made the company busier without making it more valuable. Instead, the work starts with the system. The team ranks accounts by relationship quality and finds that three industries account for the customers who stay longest and expand most. Growth roles get assigned, with the founder’s relationships documented and transitioned to named account owners. Two priority markets get chosen. An ideal customer profile gets written from the best existing accounts. A follow-up cadence goes into the CRM.

Eighteen months later, growth is tracking ahead of plan, and more important for the firm, the founder is no longer the only person who can produce it. At exit, the company sells as a business with a repeatable growth engine rather than a founder with a customer list.

How should an operating partner sequence the first 180 days?

Spend the first 90 days diagnosing and documenting the growth system, then the next 90 days installing ownership and rhythm so the leadership team can run it. The mistake is starting with activity. The right sequence starts with clarity.

In the first 30 days, do the diagnostic. Map the revenue, rank the customers, and find the pattern in the best relationships. Interview the leadership team about who owns what, and find the gaps. Resist the urge to launch initiatives before the picture is clear.

In days 30 to 90, document the system. Write the ideal customer profile, choose priority markets, and define growth roles. Get the leadership team’s agreement on each, because a system the team did not help build is a system the team will not run.

In days 90 to 180, install ownership and cadence. Put the follow-up rhythm into the CRM, transition founder-held relationships to named owners, and set the operating rhythm that keeps the system running. By the end of the window, the operating partner’s role shifts from building to coaching, and the company carries the growth function on its own.

Defined term: Operating rhythm

The recurring schedule of reviews, decisions, and adjustments that keeps a growth system running. It is owned by the company’s leadership rather than the operating partner, and it continues whether or not the firm is in the room. A healthy operating rhythm is the signal that a system has been installed rather than imposed.

What should an operating partner stop doing?

Stop being the growth engine. The most common failure mode for a capable operating partner is solving the company’s growth problems personally, because doing so feels productive and produces short-term wins. It also guarantees the gains evaporate the moment attention moves elsewhere.

Stop measuring activity as if it were progress. A busy sales team, a full calendar of check-ins, and a stack of dashboards are not the same as a company that grows on its own. Measure whether ownership has moved to the leadership team and whether the system runs without the firm.

Stop treating the value-creation plan as a forecast to monitor. A plan that lives in the firm’s files and gets reviewed quarterly is oversight. A plan installed inside the company, owned by named people and run on a documented rhythm, is a system. The second one is what compounds.

What this means for portfolio value

An operating partner who installs a growth system is building an asset the firm can sell. An operating partner who runs growth personally is renting results that end at the next transition. The difference shows up in the exit multiple and in how the diligence process reads the durability of the company’s earnings.

The companies in the lower middle market that PE firms most want to own, the established, relationship-driven businesses with loyal customers and underdeveloped growth functions, are exactly the ones where this work pays off most. They have the relationships. What they usually lack is a documented way to protect, deepen, and repeat them. Giving the leadership team that system is the highest-return thing an operating partner can do, because it turns a good company that depends on a few people into a growth business that depends on a structure.

That is the shift worth making. From overseeing growth to installing the capacity for it, and from being indispensable to making the company independent.

Ready to grow?

Help your portfolio companies install relationship-driven growth that compounds through the hold period.